A friend of ours renewed a póliza a plazo (that is a fixed-term deposit, what most expats back home call a CD) at his coop in April. He'd locked in something close to 9% two years earlier and walked in expecting the same. He walked out with an offer near 6.5% and a slightly wounded look, like the bank had personally let him down.

He hadn't done anything wrong, and neither had the bank. The number just moved. If you parked money in an Ecuadorian póliza during the good old days of 2023 and 2024 and you're staring at renewal rates now, you've probably had the same small heartbreak. So let me explain what actually happened, because the reason is more reassuring than it feels, and it hints at what to do next.

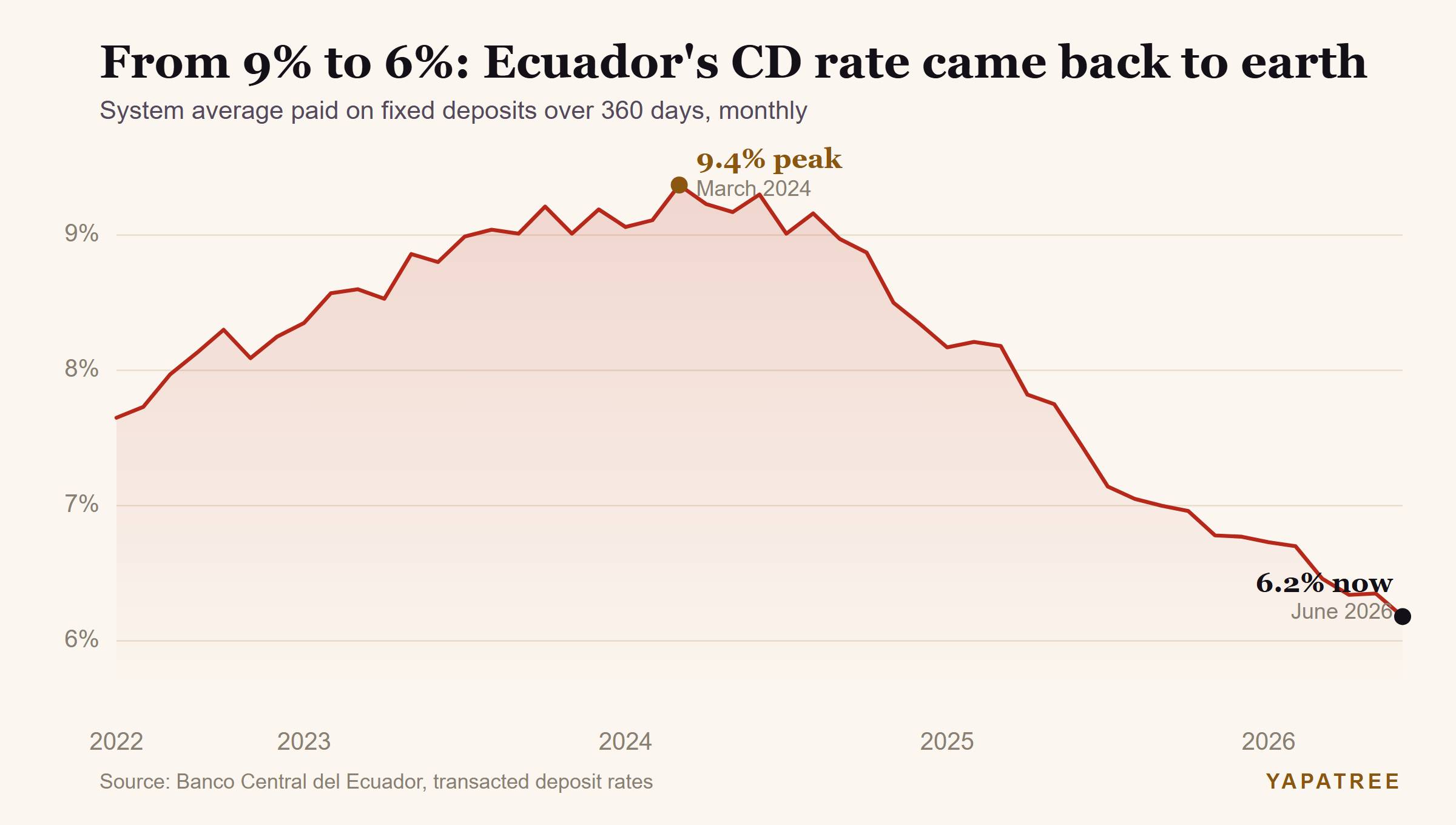

What the numbers actually did

Here is the part that can be confusing and where I see people coming unstuck. They remember a headline rate from a single coop and treat it as "the rate." The cleaner way to see it is the whole market at once.

Our own data, pulled from the Banco Central del Ecuador transacted-rate series, shows the system average for deposits over 360 days peaked at about 9.4% in March 2024. As of June 2026 that same average sits around 6.2%. This is the entire banking system repricing.

The rest of the market tells the same story. The effective average rate for savers fell from 6.8% in November 2024 to about 5% a year later. Coops still pay more than private banks, averaging about 6.92% against roughly 5.01% for private banks on fixed terms, but even that gap has come down from where it was.

Why rates were so high in the first place

To understand the fall, it helps to see why 2023 and 2024 were so high.

Ecuador was, to put it plainly, high risk money. There was a security crisis, a snap election, and then the drought that gave us the apagones, those rolling blackouts that turned many of us into UPS experts and resulted in buildings with generators becoming hot commodities. Foreign capital gets nervous in a country that looks like that, and nervous capital wants out. Banks that needed deposits to fund themselves had to fight to keep every dollar, so they paid up. On longer terms in that stretch, coops pushed toward 9.8% and banks toward 8.8%.

That is the thing to hold onto. A 9% póliza was not a sign the country was thriving. It was the country paying you a premium to sit still while everyone else panicked. Higher deposit rates rewarded you for the increased risk.

Driver one: the system got liquid again

When the fear drained out, the money came back. Between January and November 2025, deposits in private banking grew 17% year on year to about USD 59.3 billion, roughly 47% of the country's GDP, carried by strong remittance flows and better prices for non-oil exports.

This is the core mechanism, and it is boring but in a good way. A bank that is short of cash competes hard for your deposit. A bank that is swimming in cash does not need to. Once the vaults filled back up, the tasa (the rate) had nowhere to go but down. Nobody decreed it. Supply and demand did it.

Driver two: the banks can't lend it fast enough

Deposits came back faster than good borrowers did. Credit demand stayed soft and banks stayed cautious, partly because loan defaults ran high through 2024, so analysts expect passive rates to stay low through 2026.

Think about what that does to your bargaining position. A bank makes money on the spread between what it pays you and what it charges a borrower. If it is taking in deposits but struggling to put them to work in loans, every extra dollar of deposits is a cost, not an opportunity. So it has even less reason to increase the rate it pays you.

Driver three: the country stopped looking risky

The macro environment changed too. Ecuador's country risk fell below 500 basis points in December 2025, its lowest in seven years. The IMF, wrapping up its fifth program review, noted that sovereign spreads had narrowed by more than 1,300 basis points since the April 2025 election, sitting near 490 basis points, the lowest since 2018.

Two things here. First, remember Ecuador is dollarized (we adopted the US dollar back in 2000). We have no central bank printing sucres and no local policy rate to twist, so our deposit rates mostly track liquidity and risk rather than some governor's decision. Second, as the US Federal Reserve cut rates through 2024 and 2025, the cost of pulling dollars in from abroad fell, taking even more upward pressure off local rates. Lower risk plus cheaper external funding means a smaller premium paid to you, which is the repricing local analysts have described all year. That is the whole chain.

What this means for your next póliza

So you are sitting on a maturing deposit. Here is what I would tell a mate.

Ladder it, and lean longer while the premium lasts. The over-360-day bracket still pays meaningfully more than short terms right now. Splitting into staggered maturities keeps some cash reachable while you lock the longer, higher slice.

Weigh the coop premium against the coop's grade. Coops pay more for a reason: they sit a notch higher on the risk ladder than a big private bank. The deposit-insurance cap through COSEDE is USD 32,000 at qualifying institutions, so keep any single deposit under that line.

Mind the tax on shorter deposits. Interest on a deposit held 180 days or more is exempt from income tax, while one held under 180 days carries a 3% withholding, so a short term chasing a headline rate can quietly cost you. Our CD rates comparison runs the after-tax math on each term, so you compare real returns rather than headline numbers.

For live, institution-by-institution rates and the current safety grades, see our Ecuador CD rates guide. This article is the evergreen why. That page is the monthly what.

Will they fall further?

Probably they stay low into 2026, barring a shock, though a real pickup in lending could firm them back up. Nobody has a crystal ball, and anyone who gives you certainty here is selling something.

But let me balance this out. A 6.2% return in a dollarized economy, with no exchange-rate risk between you and your money, is still a genuinely good real return. It beats the roughly 4% top-tier US savings accounts pay right now, and it does it in the same currency. The 9% era was a high risk environment. What you have now is more sustainable. That is not a downgrade worth losing sleep over.

Here is your yapa for today: do not renew on autopilot the week your póliza matures. Rates move month to month, and coops and banks are not all repricing at the same speed. See the current, institution-by-institution numbers on our Ecuador CD rates page, or send us a message and we'll point you in the right direction. No hard sell, just the real figures from people who live here.

The fine print: YapaTree is a real estate agency, not a licensed financial adviser, investment firm, or tax professional. Everything above is general information for people living in or moving to Ecuador, not personalised investment, tax, or financial advice. Rates and tax rules change, deposit insurance has conditions, and your own situation is yours alone. Confirm the current numbers and, for anything that matters, check with a qualified professional before you commit real money.